KUWAIT: Continued economic growth, moderate domestic inflation and higher rates will preserve GCC banks' solid financial performance, driving a stable outlook, says Moody's Investor Service in its latest report. Higher oil prices and increased production after an OPEC+ agreement in 2021 have substantially increased hydrocarbon revenues in all six GCC countries. Crude oil output is likely to decline in 2023 after recent strategic production cuts announced by OPEC+, but hydrocarbon revenues will remain sufficiently robust for most GCC sovereigns to run substantial fiscal and current account surpluses in 2023.

This will allow governments to pay down debt, rebuild fiscal reserves, accumulate foreign-currency buffers, and progress with structural reforms and economic diversification projects. Strengthening government balance-sheets will boost confidence in the non-oil economy where banks do most of their business. Over time, more diversified economies will improve resistance against economic and fiscal shocks.

High energy prices through 2023 and ongoing economic diversification initiatives will support business sentiment in non-oil sectors where GCC banks do most of their lending. Robust capital and reserves provide protection GCC banks have robust core capital buffers against unexpected losses, and their problem loans are for the most part fully covered by provisions set against expected losses, Moody's said.

Moderate inflation

Moderate inflation and resilient economies will keep loan performance stable. Inflation will stay moderate in the GCC thanks to robust fiscal positions, tightening monetary policy and a strong US dollar. This will keep loan performance steady. Higher government hydrocarbon revenues will swell GCC banks' deposit base, while regulatory liquidity buffers will remain sound. Demand for credit in Saudi Arabia is strong as work around the government's vision 2030 megaprojects is intense and will continue to squeeze the funding base of the country's banks.

GCC banks have little direct exposure to carbon transition risks. However, the health of GCC economies tracks changes in oil prices. Oil revenue is also the main driver of government spending and of the non-oil business activity that provides the main lending opportunities for banks. Their indirect exposure is therefore higher. Hydrocarbon revenue accumulation will bolster the credit quality of GCC sovereigns in 2023, lifting business confidence.

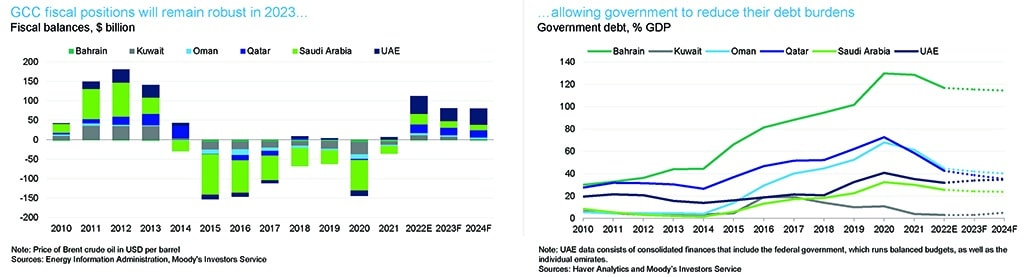

GCC fiscal position

After a peak of $102 in 2022, we expect the price of Brent crude to average $95 a barrel (bbl) this year and $90/bbl in 2024, well above the 2021 average of $70/bbl. This is because slower global growth and the related impact on hydrocarbon demand will be largely offset by a geopolitical premium to oil and gas prices stemming from the military conflict in Ukraine (Caa3, negative).

GCC governments are focused on maintaining fiscal discipline and implementing reforms to reduce oil dependence. Government spending will therefore be less expansive than in previous periods of high oil prices. In nominal terms, we expect total spending across GCC countries to increase by around 1 percent in 2023, compared with an annual average of around 12 percent during 2011-2014. Nevertheless, windfall oil revenues will preserve some level of spending, boost market sentiment and enhance the region's economic resilience.