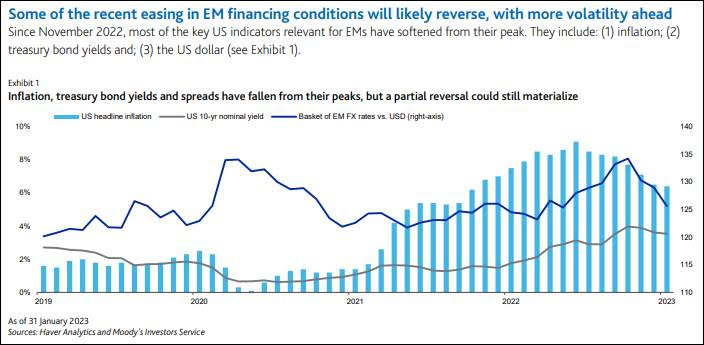

WASHINGTON: Recent improvement in financing conditions is positive for many emerging market (EM) issuers, with inflation, yields and spreads all somewhat lower since November 2022. Nevertheless, hopes for rate cuts in the US (Aaa stable) in the near term are likely misplaced, while China’s (A1 stable) rebound will not provide the same broad-based benefits as in previous cycles. Financing conditions will remain tight, with frontier economies most exposed. Some of the recent easing in EM financing conditions will likely reverse, with more volatility ahead. The recent easing partly reflects declining inflation, which has spurred expectations that the tightening cycle may have peaked. However, we continue to assume that monetary policy will remain restrictive, with rate cuts unlikely in 2023. While hopes of a more benign growth environment are increasing, the corollary of a sustained decline in inflation will be significantly lower growth.

China rebound is positive but will provide only limited, short-term benefits for most EMs. While China’s swift reopening in late 2022 is positive for China’s real GDP growth, domestic consumption is the main driver of the increase. This is positive for Asian countries with large tourism sectors but will not likely have a major effect on most other EMs. We believe China’s GDP growth will decline structurally unless there is a large pickup in productivity and consumption.

EM inflation is falling as economies respond to the decisive steps taken by central banks since 2021 and the effects of commodity prices retracting from their peak. However, growth is also set to ease for most EMs in 2023. Any accompanying increase in unemployment and social risks will pose challenges to policymaking and creditworthiness. “Elevated default risks are concentrated in a handful of frontier sovereigns. While 25 percent of rated EM sovereigns have ratings of Caa1 or below, they account for less than 10 percent of total external rated debt and some have already defaulted. For the remaining EM sovereigns that we rate, default risks are most acute for frontier economies, in particular those with lower incomes and less access to international capital markets. In contrast, larger and higher-rated EM sovereigns will continue to demonstrate the resilience they have shown in recent months. Our baseline forecast for US real GDP assumes generally flat growth with a recession in the middle of 2023, reflecting the US Federal Reserve’s determination to raise domestic interest rates high enough to bring down inflation sustainably.

While some recent economic data suggests that economic growth remains very resilient and that headline inflation has also fallen, core inflation remains elevated. Were a recession to be avoided, it would likely sustain the current positive sentiment toward EMs. This is not our baseline forecast, however. Despite the positive benefits of robust economic growth, we anticipate that EM financial conditions will continue to remain challenging for much of 2023. China rebound is positive but will provide only limited, short-term benefits for most EMs The relaxation of China’s COVID-19 control measures at the end of 2022 have provided a further tailwind for EMs.

In conjunction with a shift in policy focus to growth from regulatory tightening and deleveraging, China’s economic output in 2023 will likely be stronger than previously expected. Recent data points also suggest a strong rebound in consumption and services activity because of the reopening of borders and the Lunar New Year holiday. For example, some outbound travel bookings over this period have increased by over 600% from 2022 (according to booking sites), with the biggest benefits for neighboring Asian countries such as Thailand (Baa1 stable) and Malaysia (A3 stable). Nevertheless, we believe that infrastructure investment and manufacturing growth will moderate from the strong pace in 2022. This, together with weaker exports, will weigh on manufacturing investment and production. Furthermore, a significant unknown is whether the property market will stabilize.

Given that the measures announced so far are unlikely to stimulate a full return in market confidence, a recovery may require some time. Reflecting the above, we think a broad short-term boost to most EMs’ GDP growth will be limited. It is also notable that the increase in commodity prices (with the exception of iron ore) since China’s reopening has been relatively muted, meaning limited net benefits for most EM commodity exporters in 2023.

The primary focus for EM macro conditions in 2023 will be GDP growth rather than inflation. Throughout most of 2022, EM central banks demonstrated their ability and willingness to lower inflation and defend their currencies against excessive volatility. Most notably, central banks in Latin America and in particular, Brazil (Ba2 stable), responded earlier and more aggressively than those in advanced economies. As a consequence, inflation is generally falling in most major EM economies, including in some parts of Eastern Europe and Africa, where the effects of high energy and food prices have been particularly severe (see Exhibit 3). For most EMs, we expect inflation to trend toward central banks’ targets throughout 2023. While this would be a positive development overall, price levels still remain high in absolute terms and will continue to dent both purchasing power and growth.