Iran sanctions and record US production impact

{kind=link}

In the futures markets, hedge funds have reduced their 'net long' positions on Brent crude, the difference between bets on higher prices ('longs') and lower prices ('shorts'), for the sixth consecutive week, to 260,048 futures and options contracts, according to ICE data. This is the lowest level since July 2017, indicating that investors are turning increasingly more negative about the oil price outlook.

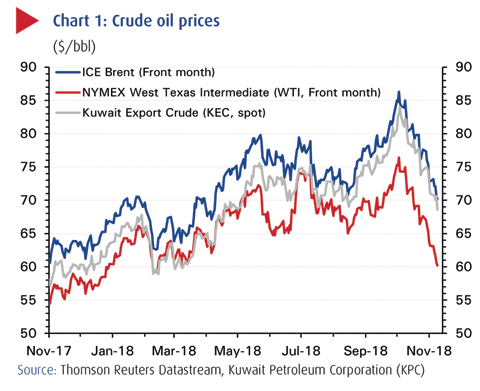

The precipitous fall in prices, in the case of WTI, by more than 19 percent to its lowest level since March, appears to have prompted OPEC to consider the option of cutting production in 2019, a complete reversal of their current trajectory.

This is a far cry from the state of the market in the run up to oil's peak at $86 in early October. That rise capped a two-month price rally that was driven primarily by concerns of a global supply shortage caused mainly by the US sanctions on Iran and falling output from Venezuela.

There were also doubts about Saudi Arabia and OPEC's ability to tap into spare production capacity to offset these losses, as shown by the slower-than-expected ramp up in output from OPEC and its allies after they had indicated in late June that they would pump an additional 1 mb/d over the coming months to keep the market well-supplied. The slow pace of supply additions while the price of Brent increased towards its eventual peak even drew the ire of President Trump, who accused OPEC of intentionally "ripping off the rest of the world".

Iran sanctions kick in

On 5 November, US sanctions on Iran went into full effect. In all, about seven hundred Iranian entities, including individuals, banks and businesses, across the country's energy, shipping and financial sectors were targeted. Henceforth, foreign countries and entities purchasing Iranian crude without special US dispensation or transacting with the Islamic Republic's central bank will be effectively barred from doing business using the US financial system-a penalty that has forced Iran's largest crude customers to pare back purchases and firms such as France's Total to pull out of a planned $4.8 billion natural gas development project in the country. The international payments enabler, SWIFT, also announced that several Iranian banks will have their access to the platform suspended.

However, in a surprise move on the eve of the sanctions 'snap-back', the Trump administration, announced that eight of Iran's largest crude oil customers, including China, India, South Korea and Japan-but not the EU as a single entity-would be offered temporary waivers to allow them sufficient time to cut their imports down to zero, the administration's stated objective. The EU, for its part, continues to hold out hope that its plans for a special payments vehicle to help Iran bypass the US financial system and continue exporting to Europe and Asia will materialize.

Implicit in the US's softer Iran stance is the Trump administration's anxiety over spiking oil prices and the effect on the US consumer both ahead of and after the US midterm elections. But the markets also took the move as a signal that the projected loss of Iranian crude may not be so severe as to leave the markets short of barrels.

To be sure, Iranian crude exports continue to fall. The most recent figures show the crude exports at 1.6 mb/d in October, a decline of 926,000 b/d, or 37 percent, from the country's peak export volume of 2.4 mb/d in April, the month before the US announced its intention to re-impose sanctions. (Chart 3.) Though the rate of decline has eased somewhat over the last two months-and may continue to do so now that the waivers have been issued-the expectation is that the regime's crude exports will probably fall back over the next few months to the previous sanctions-era levels of around 1-1.2 mb/d.

OPEC finally opens the taps

OPEC has finally increased its output to compensate for Iranian and Venezuelan losses. The group's crude production reached 32.7 mb/d in September, an increase of 630,000 b/d over May's levels. Adding in Russia's output gain of 390,000 b/d over the same period, then OPEC and its allies are not far off the 1 mb/d they had promised in late June. Saudi Arabia, for its part, ramped up production in September by 500,000 b/d to 10.5 mb/d, close to its all-time high of 10.67 mb/d from November 2016.

Kuwait and the UAE produced around 2.8 and 3.0 mb/d in September, respectively, according to OPEC secondary sources, which brings their respective incremental increases from May to 110,000 b/d and 140,000 b/d. The Saudi energy minister, Khaled Al-Falih, remarked recently that OPEC is in "produce as much as you can mode", with Saudi Arabia looking at possibly 11 mb/d or higher over the coming months. All the indications are that those oil producers with the spare production capacity-Saudi Arabia, Iraq, Kuwait, the UAE and non-OPEC Russia-intend to increase supplies in the short term.

While a thinning Saudi and OPEC spare oil production capacity buffer-estimated at around 2 percent of global demand, which is low by historical standards-would ordinarily sound the alarm bells as far as the markets are concerned, the focus appears to have shifted to the risk that the market could tip into oversupply.

Oversupply concerns

These concerns were recently aired by both the Saudi energy minister and the Saudi OPEC governor. Both alluded to surging shale-led production in the US and rising US crude stockpiles amid weakening slowing global demand growth.

In the US, crude output set another all-time high record in recently, reaching 11.6 mb/d in the week-ending 2 November, according to weekly data from the US Energy Information Administration (EIA). US crude production has now surpassed both Russia and Saudi Arabia as the largest in the world, surging by an incredible 1.8 mb/d, or 19 percent, in 2018 so far. US crude stocks also notched up a seventh consecutive week of increases, to reach 431.8 million barrels.

Oil market already in surplus

In fact, according to the IEA, oil supply has exceeded oil demand in every quarter of this year, with more noticeable stock builds occurring over the second and third quarters of the year. Saudi oversupply concerns, therefore, appear to have some substance.

Moreover, on the current supply trajectory, the situation is not likely to improve in 2019. Not only were oil demand growth projections brought down this year, by 130,000 b/d to 1.3 mb/d, but the IEA has also cut its forecast for 2019, by 200,000 b/d to 1.4 mb/d.

The agency cited a combination of higher oil prices, downward adjustments to Chinese data and weaker global economic growth, as projected by the OECD and the International Monetary Fund (IMF).

Higher oil prices combined with significant currency depreciation in emerging markets stemming from rising US interest rates and some capital 'flight to quality'-risks the IMF identified in their October WEO- have raised the domestic cost of oil products in several emerging markets. In India, for example, which has seen its currency decline by almost 15 percent this year against the dollar, the authorities had to reduce domestic gasoline and diesel prices in early October to mitigate the impact on households.

Even in the US, higher pump prices for the consumer are beginning to affect demand for gasoline. Gasoline's share of total US oil demand is significant at 44 percent, but according to weekly August and September figures, gasoline demand has been contracting.

Weighing on the outlook for next year in addition to tighter US monetary policy is the possibility of heightened trade friction between the US and China. Oil demand would naturally be impacted were an escalation in trade tariffs to occur and result in slower global economic growth. The IMF lowered its global growth estimate for 2018 and 2019 by 0.2 percentage points to 3.7 percent, in part to reflect these downside risks.

Where now for oil prices?

The balance of risks appear skewed to the downside as far as oil prices are concerned. The markets seem to be attaching greater weight to surging OPEC and US crude production, rising stockpiles and weaker economic growth ahead than they are to the possibility that Iranian sanctions and declining Venezuelan production will lead to a shortage of oil. Prices for future Brent oil deliveries are lower than for immediate, or spot, deliveries. Known as backwardation, this state suggests that traders expect the market to have a surfeit of supply.

Of course, if OPEC and its partners were to reverse course in 2019 and cut production rather than increase it, then the landscape could change dramatically. All in all, the only thing certain in this market may be more volatility.

NBK ECONOMIC REPORT

Head Office

International Network

NBK Capital

Kuwait

National Bank of Kuwait SAKP

Abdullah Al-Ahmed Street

P.O. Box 95, Safat 13001

Kuwait City, Kuwait

Tel: +965 2242 2011

Fax: +965 2259 5804

Telex: 22043-22451 NATBANK

www.nbk.com

Bahrain

National Bank of Kuwait SAKP

Zain Branch

Zain Tower, Building 401, Road 2806

Seef Area 428, P. O. Box 5290, Manama

Kingdom of Bahrain

Tel: +973 17 155 555

Fax: +973 17 104 860

National Bank of Kuwait SAKP

Bahrain Head Office

GB Corp Tower

Block 346, Road 4626

Building 1411

P.O. Box 5290, Manama

Kingdom of Bahrain

Tel: +973 17 155 555

Fax: +973 17 104 860

United Arab Emirates

National Bank of Kuwait SAKP

Dubai Branch

Latifa Tower, Sheikh Zayed Road

Next to Crown Plaza

P.O.Box 9293, Dubai, U.A.E

Tel: +971 4 3161600

Fax: +971 4 3888588

National Bank of Kuwait SAKP

Abu Dhabi Branch

Sheikh Rashed Bin Saeed

Al Maktoom, (Old Airport Road)

P.O.Box 113567,Abu Dhabi, U.A.E

Tel: +971 2 4199 555

Fax: +971 2 2222 477

Saudi Arabia

National Bank of Kuwait SAKP

Jeddah Branch

Al Khalidiah District,

Al Mukmal Tower, Jeddah

P.O Box: 15385 Jeddah 21444

Kingdom of Saudi Arabia

Tel: +966 2 603 6300

Fax: +966 2 603 6318

Jordan

National Bank of Kuwait SAKP

Amman Branch

Shareef Abdul Hamid Sharaf St

P.O. Box 941297, Shmeisani,

Amman 11194, Jordan

Tel: +962 6 580 0400

Fax: +962 6 580 0441

Lebanon

National Bank of Kuwait

(Lebanon) SAL

BAC Building, Justinien Street, Sanayeh

P.O. Box 11-5727, Riad El-Solh

Beirut 1107 2200, Lebanon

Tel: +961 1 759700

Fax: +961 1 747866

Iraq

Credit Bank of Iraq

Street 9, Building 187

Sadoon Street, District 102

P.O. Box 3420, Baghdad, Iraq

Tel: +964 1 7182198/7191944

+964 1 7188406/7171673

Fax: +964 1 7170156

Egypt

National Bank of Kuwait - Egypt

Plot 155, City Center, First Sector

5th Settlement, New Cairo

Egypt

Tel: +20 2 26149300

Fax: +20 2 26133978

United States of America

National Bank of Kuwait SAKP

New York Branch

299 Park Avenue

New York, NY 10171

USA

Tel: +1 212 303 9800

Fax: +1 212 319 8269

United Kingdom

National Bank of Kuwait

(International) Plc

Head Office

13 George Street

London W1U 3QJ

UK

Tel: +44 20 7224 2277

Fax: +44 20 7224 2101

National Bank of Kuwait

(International) Plc

Portman Square Branch

7 Portman Square

London W1H 6NA, UK

Tel: +44 20 7224 2277

Fax: +44 20 7486 3877

France

National Bank of Kuwait

(International) Plc

Paris Branch

90 Avenue des Champs-Elysees

75008 Paris

France

Tel: +33 1 5659 8600

Fax: +33 1 5659 8623

Singapore

National Bank of Kuwait SAKP

Singapore Branch

9 Raffles Place # 44-01

Republic Plaza

Singapore 048619

Tel: +65 6222 5348

Fax: +65 6224 5438

China

National Bank of Kuwait SAKP

Shanghai Office

Suite 1003, 10th Floor, Azia Center

1233 Lujiazui Ring Road

Shanghai 200120, China

Tel: +86 21 6888 1092

Fax: +86 21 5047 1011

Kuwait

NBK Capital

38th Floor, Arraya II Building, Block 6

Shuhada'a street, Sharq

PO Box 4950, Safat, 13050

Kuwait

Tel: +965 2224 6900

Fax: +965 2224 6904 / 5

United Arab Emirates

NBK Capital Limited - UAE

Precinct Building 3, Office 404

Dubai International Financial Center

Sheikh Zayed Road

P.O. Box 506506, Dubai

UAE

Tel: +971 4 365 2800

Fax: +971 4 365 2805

Associates

Turkey

Turkish Bank

Valikonagl CAD. 7

Nisantasi, P.O. Box. 34371

Istanbul, Turkey

Tel: +90 212 373 6373

Fax: +90 212 225 0353

(c) Copyright Notice. The Economic Update is a publication of the National Bank of Kuwait. No part of this publication may be reproduced or duplicated without the prior consent of NBK.

While every care has been taken in preparing this publication, National Bank of Kuwait accepts no liability whatsoever for any direct or consequential losses arising from its use. GCC Research Note is distributed on a complimentary and discretionary basis to NBK clients and associates. This report and other NBK research can be found in the "Reports" section of the National Bank of Kuwait's web site. Please visit our web site, www.nbk.com, for other bank publications. For further information please contact: NBK Economic Research, Tel: (965) 2259 5500, Fax: (965) 2224 6973, Email: econ@nbk.com