KUWAIT: Official consumer, monetary and banking data in the first quarter of 2023 continued to signal a normalization in Kuwait’s non-oil economy post-pandemic. Closely watched leading indicators such as consumer spending, real estate sales and bank credit point to a moderation in non-oil activity amid still-elevated inflation, tighter monetary conditions and softening global macroeconomic conditions. Surprising on the upside in 1Q23, however, was the uptick in project activity, suggesting some increased momentum albeit from a very low base.

The recovery in expatriate numbers in 2022, as seen in the official PACI population data, many of which will likely work on projects, further fleshes out a macroeconomic picture that is still fairly positive despite the more challenging conditions. This included in 1Q23 the resurfacing of troubles in the political sphere, which eventually culminated in the resignation of the government and a Constitutional Court ruling that voided the 2022 national assembly on procedural grounds and reinstated its predecessor. The 2020 parliament has since been dissolved by Amiri decree and fresh elections have been called for 6 June.

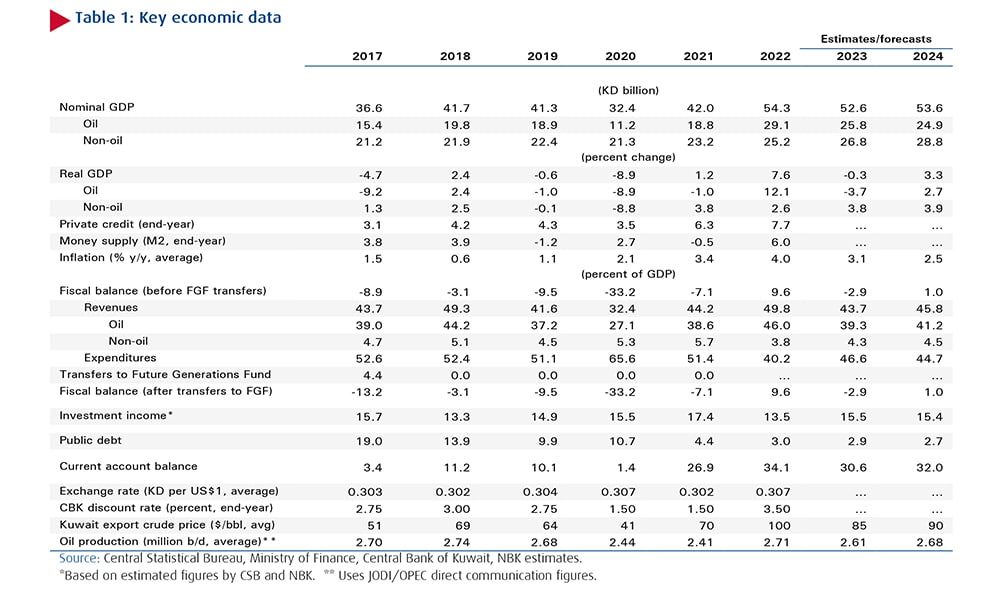

Anxieties over the trajectory of global economic growth in 2023 hammered oil prices, forcing several OPEC+ members including Kuwait to roll out further production cuts from the beginning of May over and above those approved last October. Real oil GDP for the year has therefore been revised down. Moreover, were oil prices to remain at current levels which is not our expectation for the year, government fiscal policy may need to readjust, such that spending increases of the magnitude outlined in January’s expansionary but still-to-be approved draft budget may be trimmed back.

Oil posts third quarterly loss

Oil prices were subjected to intense downward pressure in 1Q23 over market fears of an economic slowdown amid central bank rate hikes, stubborn inflation and bank failures in the US and Europe. Brent front month futures closed down 7.1 percent ytd at $79.8/bbl in March, having fallen to a 15-month low of $72.9/bbl earlier in the month. Local marker Kuwait Export Crude also posted its third quarterly decline, closing down 3.3 percent q/q at $79.3/bbl by quarter’s end.

With bearish sentiment in the ascendancy and China’s post-COVID economic rebound still in its infancy, several OPEC+ members including Kuwait, Saudi and the UAE announced in early April additional, voluntary production cuts totaling around 1.2 mb/d effective May through to December. For Kuwait, the reduction in output amounts to 128 kb/d and a new quota of 2.55 mb/d. The OPEC+ announcement initially had its intended effect, arresting the decline in prices and then propelling them to a high of $87/bbl by mid-April. The gains were transitory, however, and prices have mostly been in retreat ever since, struggling to shake off intensifying fears of a global recession—even while the physical market continued to signal some tightness amid successive US crude inventory draws, increased refining throughputs in China and suspended Kurdish oil exports. Despite the near-term macroeconomic anxieties, we still see the oil market tightening significantly in 2H23 and prices firming from current levels (to an average of $85/bbl in 2023) after OPEC+ output cuts filter through and after China’s economic rebound starts gaining traction.

Figures published by the Central Bank of Kuwait (CBK) show the value of credit and debit card transactions (a proxy for consumer spending) increasing by a robust 13.8 percent y/y(3.8 percent q/q) in 1Q23. Local spending growth slowed to 13.4 percent y/y from 14.7 percent in 4Q22, while overseas spending grew by 19.8 percent y/y from 6.9 percent in the previous quarter.

While still solid, the data nevertheless reinforces our view that activity is normalizing after the post-pandemic surge and against a backdrop of stubbornly elevated inflation and higher borrowing costs. We think spending growth could moderate further ahead, though could also be supported by the government’s expansionary but still-to-be-approved draft budget for FY23/24.

Real estate activity softens

In the real estate sector, demand has been moderating as the post-pandemic boom abates and activity returns to more normal levels. High valuations in the residential sector, rising borrowing costs and an uncertain macroeconomic and policymaking environment—especially over utility subsidy reforms and government land distributions—have all contributed to the slowdown. Total real estate sales slipped to KD 714 million in 1Q23 (-15 percent q/q; -20 percent y/y), the lowest level since 3Q20.

Residential (-24 percent q/q) and investment (-5.3 percent q/q) sector activity both declined, while commercial sales (+5.5 percent q/q) rose. Seasonal factors, such as the holy month of Ramadan, part of which extended into the annual comparison, may also have contributed to the easing in activity compared to last year, since the volume of transactions was noticeably down (-34 percent y/y). The price of real estate (both residential and investment properties) may have fallen in Q1, though was still up 4.7 percent y/y.

Our base case outlook for real estate activity in 2023 is one of continued moderation, especially amid softening local and international macroeconomic conditions. Increased plot distributions could help stimulate activity, though. The Kuwait Savings and Credit bank (SCB), through which plots are allocated and housing loans are granted, has requested an additional capital increase of KD 275 million to meet the ever-increasing backlog of outstanding applications (90,915 as of March 2023). If approved, this could also help speed up and stimulate activity in the sector.

The long-awaited mortgage law, although not expected this year, would also boost activity and real estate lending once implemented.

Project awards surged in 1Q23, the second quarterly increase in a row, with the value of awarded contracts topping KD 527 million (+78 percent q/q; +332 percent y/y).

The acceleration was mainly due to awards by the Ministry of Electricity & Water and Public Authority for Housing. Only three months into 2023 and the cumulative figure is already equivalent to almost three-quarters of the full value of awarded projects in 2022. MEED Projects has penciled in KD 8.4 billion worth of projects for 2023, which, if realized, would be a substantial improvement on last year. Admittedly, about half of that figure relates to KIPIC’s Al-Zour Petrochemicals Complex (KD 2.9 billion) and Kuwait Authority for Partnership Projects’ Al-Zour North Independent Water and Power project (KD 1.2 billion). Kuwait’s projects market would benefit immensely from a government and parliament firing on all cylinders, helping to minimize bureaucratic delays including in the procurement of labor and raw materials.

Inflation proves sticky

Consumer price inflation rose to 3.7 percent y/y at end-1Q23 from 3.2 percent in December. Price rises in the food (+7.5 percent y/y; +1.3 percent q/q) and housing (+2.5 percent y/y; +1.1 percent q/q) components accounted for 57 percent of the y/y inflation rate, but on the whole price gains have been broad-based; the core rate (excluding food and housing) was back up at 3.1 percent in March from a 2022-low of 2.6 percent last November. The stickiness in the inflation print points to still-solid consumer demand even as the rate of growth in consumer activity across metrics such as cards spending, credit demand and real estate sales is one of moderation. The effects of previous monetary tightening are also likely still filtering through the system. We see inflation averaging 3.1 percent in 2023, down from last year’s 4.0 percent.

Population

According to the latest demographic data from the Public Authority for Civil Information, Kuwait’s population rebounded during 2022, increasing by 8.0 percent y/y to 4.74 million. This is the fastest annual growth in 17 years and brings the total population back to just 0.8 percent below its pre-pandemic peak in 2019. The main driver was the return of expatriate workers (+11.1 percent y/y) after two years of pandemic-linked decline. The annual increase in Kuwaiti nationals eased to 1.9 percent in 2022. The growth rate of the Kuwaiti population may slow further over the coming years as the birth rate remains on a moderating trajectory. Overall expatriate employment in several labor-intensive sectors, such as real estate & construction, manufacturing and trade, continues to range below its 2019-peak; any pick-up in economic activity should therefore mean more demand for workers. Meanwhile, the number of expatriate domestic workers reached a record 772,000.

2022/23 fiscal balance to see first surplus in eight years

Amid elevated oil prices, Kuwait’s fiscal position improved greatly over the fiscal year just ended (FY22/23). According to our estimates, the fiscal balance swung to a surplus of KD 5.2 billion (9.6 percent of GDP), versus a deficit of KD 3.0 billion (7.1 percent of GDP) a year before. If confirmed by the Ministry of Finance, this would be Kuwait’s first surplus in eight years. Our estimate is based on the government limiting expenditure growth that year to 1.5 percent y/y.

In contrast, in the FY23/24 draft budget, which will need to be ratified by the incoming parliament, expenditures are projected to increase a hefty 12 percent y/y (budget-on-budget) to KD 26.3 billion alongside expectations of a sizeable 17 percent decline in revenues to KD 19.5 billion (based on a $70/bbl oil price assumption). This could result in the reversal of last year’s expected surplus to a deficit of KD 6.8 billion (13 percent of GDP).

We note, however, that almost half of the planned expenditure increase relates to non-recurring payments (electricity subsidy arrears and accumulated employee salary leave compensation) and so there could theoretically be scope for current spending to ease back in future budgets. Given the historical tendency of the government to underspend on its budget allocation (especially on capex) and to base its spending on a conservative oil price assumption, we think the FY23/24 deficit could come in at about 3.0 percent of GDP in FY23/24 (zero if the non-recurring items are stripped out). The cancellation of the current legislative session and fresh parliamentary elections will have likely delayed further sign-off on bigger ticket expenditure items.

Softening credit growth, especially household

Domestic credit growth slowed to 5.1 percent y/y in March (+0.6 percent q/q), a third consecutive month of deceleration and a marked slowdown from the double-digit increase of H1 22. Credit to the household and business sectors has noticeably eased, to 6.7 percent y/y (-0.1 percent q/q) and 4.2 percent y/y (+1.2 percent q/q), respectively, as the operating environment normalizes (household and business credit were up 9.0 percent and 6.8 percent, respectively, in 2022) against a background of higher interest rates and lower price-competition among banks in terms of household credit especially. Meanwhile, slower lending to real estate companies—credit actually contracted m/m in three of the last four months—is one of the main factors behind the slowdown in business credit growth. Industry, construction and other services, in contrast, grew by a decent 3.0 percent q/q.

Looking ahead, business credit growth is unlikely to accelerate without considerable traction in the projects market, which in turn would likely depend on the return of a new government and an uptick in oil prices from current levels. That said, the rate-hike cycle could be nearing its end, which could give corporates a little more certainty over their borrowing costs and lenders some impetus to expand corporate credit lines given weaker household credit demand.

As of May, the CBK has hiked the discount rate by a cumulative 2.5 percent since March 2022 to 4.0 percent. This compares to a cumulative increase of 5.0 percent in the US Fed funds rate to 5.25 percent at the upper limit. Following its most recent 25 bps increase in early May, the Fed may pause its rate hiking cycle, and the indications are that both the Fed and the CBK are close to or have reached the terminal rate in the current cycle.

Equities trended lower in Q1 23 amid rising borrowing costs and oil market volatility, which weighed on investor sentiment. Prices fell further in April and early May. The end of the earnings season and stocks going ex-dividend also added to the mood. Boursa Kuwait’s All-Share Index lost 3.2 percent q/q in Q1 23 to settle at 7,051 at end-March, in line with declines in regional markets (the MSCI GCC dropped 3.0 percent q/q).

Performances diverged in recent weeks, however, with Kuwaiti stocks extending losses—breaking the critical 7,000 level and touching lows unseen since November 2021—while GCC peers recovered better amid easing monetary headwinds and inflation as well as oil price-supportive OPEC+ policy. The underperformance could be attributed to domestic factors, including political uncertainty and the general absence of a catalyst.

Furthermore, turnover by value fell to just KD 642 million in April, the lowest since July 2020, indicative of increased uncertainty and risk aversion, while market capitalization fell to KD 45.6 billion from a high of nearly KD 50 billion in November. Looking ahead, Kuwait’s equity market will continue to take its cues from global economic and market developments as well as from signs of an improving political backdrop, potentially after June’s elections.