{kind=link}

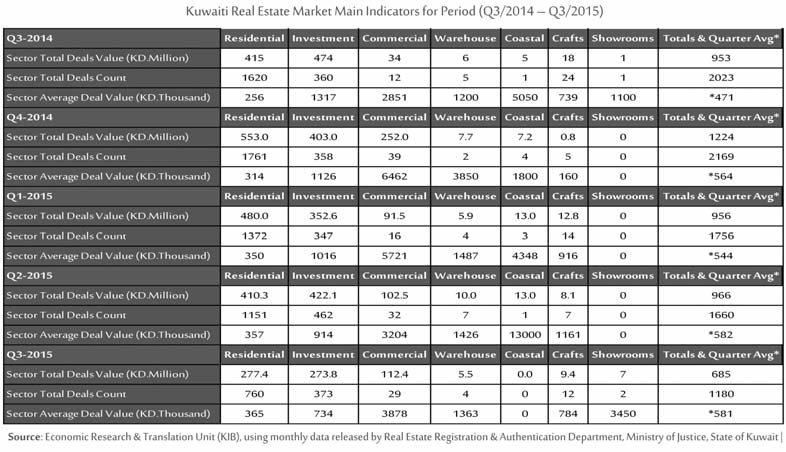

KUWAIT: The 3rd Quarter Real Estate Report issued by Kuwait International Bank indicated that Kuwait real estate market indicators slumped down for seasonal reasons and partially for global economic developments. The total sales dropped approximately by 29 percent realizing only Kuwaiti Dinar 685 million (contracts and power of attorneys). This has come as a result of a drop in the count of total deals concluded in the market to 1180 only compared to 1660 deals during Q2 of 2015. The average deal value in Q3 2015 maintained the same level recorded for the previous quarter that is around KD 581 thousand per deal. However, it is worth to mention that a large portion of this drop is due to seasonal reasons as these data coincided with summer holidays, the holy month of Ramadan, Eid Al-Fitr and Eid Al-Adha in the same current quarter, the matter which contributed in the market overall slump.

Having compared this quarter performance with the corresponding quarter in 2014, the total sales dropped by 28 percent and the count of deals went also down by approx. 42 percent. However, the average deal value increased by approx. 23 percent on annual basis. Thus, the market levels are still far away from the levels recorded for the same period last year. The real estate market sales in the first nine months of the year amounted to KD2.6 billion, ie 53.6 percent of total sales of 2014 and 72 percent of sales for the same period in 2014. The total count of deals concluded during the first nine month of this year is 4596 deals, i.e. 56 percent of total deals recorded in 2014 and 75 percent of deals registered during the same period last year. The average deal value for the first nine months is still below the recorded average deal value during 2014.

Market performance by sector

Having reviewed the real estate performance by sector, the residential and investment sectors' sales bounced back, while the commercial sector's sales rose. As such, the residential sector sales amounted to KD277 million only, decreasing by 33 percent quarterly and annually alike. The residential sector recorded 760 deals, slumping down by 34 percent quarterly and by more than 53 percent on annual basis. In Q3 of 2015, the average deal value in the residential sector amounted to KD 365 thousand, recording an increase by 2.4 percent quarterly and 43 percent on annual bases.

The investment sector's sales dropped by 35 percent quarterly and by more than 43 percent annually, realizing KD273 million. The total count of deals recorded in the investment sector during the current quarter reached 373 deals only, which is a drop by 19 percent q/q. However, the count of deals in this sector remained higher than the count registered for the same period of 2014 by 3.6 percent. The average deal value in the sector amounted to KD734 thousand decreasing by 20 percent quarterly and by more than 44 percent on annual bases.

Unlike the slumping-trend witnessed at the aforementioned two sectors, the commercial sector sales improved realizing KD 112 million, with an increase of "10 percent" q/q. The commercial sales level in this quarter is higher by more than two times the levels recorded for the same period in 2014. In turn, the deals count bounced back q/q by 9 percent with 29" deals only. Yet still higher than the deals count recorded for Q3 of 2014 which was 12 deals only. The average deal value in the commercial sector increased by 21 percent q/q and 36 percent y/y, realizing KD 3.9 million average deal values. As for the other sectors, the warehouse sector sales decreased to KD5.5 million, while the crafts sector sales increased to KD9.4 million. The showrooms sector recorded only two deals for a total value of approx. KD 6.9 million. Nevertheless. Having reviewed the promotional share of the main sectors to total market sales, the investment sector share bounced back to 40 percent only of the total market sales. While the residential sector share retreated to nearly 40.5 percent. On the other hand commercial sector share rose up to 16.4 percent. However, the other sectors share realized to 3.2 percent of the market sales during Q3 2015.

Geographical performance

Having analyzed Q3 2015 data, it is established that Hawally governorate acquired the largest share of total sales with more than 29.4 percent, i.e. KD "185" million. Al-Ahmadi Governorate came the second with 21 percent of the market total sales that is KD 134 million. Lastly, Al-Jahra total sales amounted to approx KD 29 million only.

Based on an analysis of market performance according to geographical areas, it can be noticed that Salmiya came first with 13 percent of total market sales i.e. KD 83 million whereas Mahboula was the second with approx. 6.5 percent of the total market sales. Nevertheless, Mahboula was the first in terms of count of deals with 19 percent of total.

Variant Changes in prices

Having perused the price levels in the three main sectors (residential, investment and commercial), it was obvious that prices were relatively stable in the residential sector while the average squared meter price in the investment and commercial sectors retreated. The fluctuation of prices is also attributable to the Governorate and the geographical area, whereby, the residential sector prices dropped at Al-Jahra, Farwaniya and Hawally governorates, while Al-Ahmadi governorate recorded minor drawback.

On the contrary, the residential real estate prices at Capital and Mubarak Al-Kabeer Governorates increased. The noticeable drawback of investment real estate average prices at Ahmadi Governorate led to declined average price rate in this sector in general. In addition, the fallback of commercial sector prices at Farwaniya Governorate lead the overall decline in the Commercial sector average prices. It should be notes that the estimated price levels do not take into account the individual specifications of each property.

Fallback

The fallback of Kuwait real estate indicators is attributable to seasonal and other economic reasons. The 3rd quarter of 2015witnessed several global economic developments and challenges. The market encountered a severe slump in oil and primary commodities' prices for several consecutive months; China devalued its currency by 2 percent. The matter which was followed by indications of slowdown in the Chinese economy , thus casted shadows on the performance of global money markets; the oil prices dropped to their minimal levels for the last six years continuously till end of September. This has caused temporary fear overwhelming the global money markets as well as losses by tens of billions of dollars on a day called the Black Monday (24/8/2015) before being recovered gradually.

During this period of increased concerns from the impact of the Chinese economy slowdown on the recovery of truly fragile international economy, the Federal Reserve Board decided to defer any measures pertinent to raising interest rates waiting for potential positive indications on the performance of the US economy. This has relatively and indirectly affected the performance of the local real estate market as the global economic developments always have an impact on the local economy outlook, particularly with respect to the crude oil prices.

The prevailing trend in the market represented by a drawback in both the count of deals and the total sales volume still exist while the average deal value proportionally maintained the same level, with a varying price levels due to the nature of property specifications and their detailed geographical locations. However, the average price levels are still below the prices recorded by the end of 2014.

The market performance is expected to maintain its current levels till end of 2015 unless an international positive economic development emerged to positively reflect on the local market performance in the short run, in a way that mitigate the sentiment effect prevailing in the market.