Strong dinar helps limit rising import price pressures

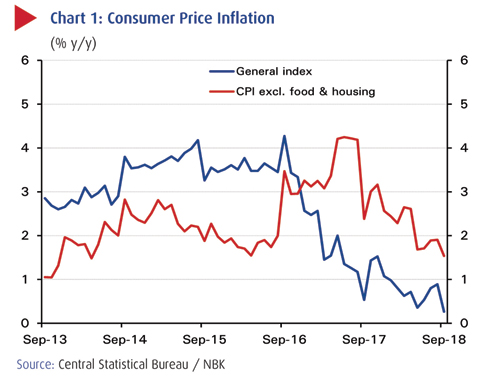

KUWAIT: Inflation hit a 14-year low of 0.3 percent y/y in September, having averaged 0.8 percent in July and August. The low September reading was driven primarily by softer food and beverage prices, and deflation in housing services (rents). But our core measure of inflation, which excludes food and housing, also eased in 3Q18, ending the quarter at 1.5 percent from 1.7 percent in June, mostly on softer inflation in services. Continued low inflation may have been helped by the stronger Kuwaiti dinar this year due to the appreciating US dollar, in turn limiting import price pressures. But it also reflects moderate rates of economic growth, soft lending growth, gradually rising interest rates and the absence of fresh subsidy cuts or increases in indirect taxes. We expect inflation to remain low in Q4 and average 0.6 percent in 2018 as a whole.

Housing services prices

Inflation in housing services eased further into negative territory in 3Q18, ending the quarter at -1.5 percent from -0.9 percent in June. But the decline was caused entirely by higher prices in the base period of last year, with rents unchanged since 2Q18. Rents are likely to remain subdued in the near term, as landlords will be reluctant to raise rents with apartment vacancy rates still high. However, there are tentative signs of improvement in the housing market reflected in a recent rise in apartment and building prices which had previously fallen a long way. But at the same time, renewed pressure on rents could occur from the introduction of new buildings and apartments that are currently under construction.

Inflation in goods picks up

Food and beverage inflation picked up from 0.1 percent y/y in June to above 1 percent in July and August but then eased to 0.4 percent in September. The spike in July/August was due to a local factor, fish and seafood prices, which are typically volatile and subject to seasonality. This price surge has since eased, bringing food inflation back to the near-zero levels commonly seen since mid-2016. Meanwhile, inflation in other goods has also risen modestly, with clothing and footwear deflation moderating to -1.4 percent in September from -2 percent at the close of 2Q18. Household goods inflation has also gradually picked up to register 2.2 percent in September from 1.9 percent in June. This could be due to summer sales coming to a close.

Inflation in services eased in 3Q18, mainly on the back of the softness in housing inflation described above. However, the drop was also due to softer prices for other services, where despite rebounding to -1 percent from a low of -2.2 percent in August, inflation is still down from the -0.4 percent recorded at the end of Q2. Services prices have generally been trending lower in 3Q18, with softer inflation evident in transportation, recreation, education, and restaurants and hotels, which together account for about 20 percent of the CPI basket.

From a forecast average of 0.6 percent in 2018, inflation is expected to pick up towards 2 percent next year. With building and apartment prices showing tentative signs of recovery, it is reasonable to expect that rents will eventually stabilize and could then begin to rise. The uptrend in global food prices may also eventually reflect on local prices. Moreover, the general economic climate is supportive of slightly firmer inflation, with oil prices still above last year's levels and GDP growth expected to rebound to 4 percent in 2019, making way for a stronger fiscal position, which may translate into higher government spending and wage growth. Finally, the central bank's recent relaxation of consumer lending limits could lift consumer spending. However there are also some continued sources of downward pressure on inflation, including rising interest rates, weak growth in the expatriate population and the strong Kuwaiti dinar, which is currently up around 5 percent against the euro and pound year-to-date, and should help limit rising import price pressures.

NBK ECONOMIC REPORT