{kind=link}

Kuwait's non-oil sector growth forecasts revised down marginally

KUWAIT: August was a tough month for many emerging markets, with sharp falls in both currency and equity markets triggered by the escalating US-China trade war and concerns over tightening global liquidity. Kuwait - along with most other Gulf countries - was largely spared the sell-off, with equities only fractionally lower and currency markets stable. Although we have revised down our forecasts for Kuwaiti non-oil growth recently, this largely reflects weaker outturn GDP data for last year rather than a change in view, and overall growth has been revised up on recent oil market strength. Indeed, the rise in oil prices has improved the fiscal outlook and it looks possible that the budget could be close to balance this year.

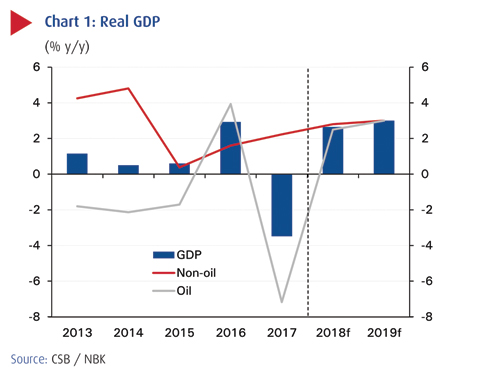

Revised 2017 GDP data

Revised GDP data show that economic growth was weaker than previously thought last year, at -3.5 percent versus the initial estimate of -2.9 percent. The fall in oil sector production of 7.2 percent - driven by OPEC policy-led cuts in oil output - was actually milder than the previous estimate of an 8.0 percent decline. But this was more than offset by the non-oil sector, where growth was revised down to 2.2 percent from 3.3 percent before. Non-oil growth in 2017 was weighed down by weakness in the construction sector where output dropped 12 percent y/y, perhaps related to softness in the real estate market. But there were strong performances by the hospitality (11 percent), transport (5 percent) and telecoms (5 percent) sectors.

More recent data for 1Q18 show non-oil growth at 3.1 percent y/y, stronger than at the end of last year. And in general, we continue to believe that the economic backdrop is gradually improving, given the continued recovery in government spending after earlier cuts, stronger regional growth and especially the upward revision to our oil price forecast (see below). However, we have recalibrated our growth forecast with the new, softer data for 2017 and now expect non-oil growth of 2.8 percent this year and 3.0 percent next versus 3.5 percent before. Incorporating upgrades to our oil sector growth (see below), total GDP is now forecast at 2.6 percent and 3.0 percent, respectively, in 2018 and 2019.

Oil prices and production

Crude oil prices rallied in the second half of August, with Kuwait Export Crude ending the month up 3 percent at $75/bbl and in early September hitting a new four-year high of just below $76. Although there was concern over the impact of US-China trade tariffs and emerging market currency crises, the outlook for oil demand remains reasonably solid. Meanwhile, however, there were reports that Iranian oil exports had dropped by an unexpectedly large 0.6 million b/d following the restart of US sanctions, implying the need for higher output from other OPEC members to help balance the market. Prices have averaged $69/bbl so far this year, up around one-third from the average for 2017, and based upon this strength and the continued risk of supply disruptions, we have revised up our forecasts for KEC to $69 and $67/bbl this year and next ($72 and $70 for Brent), from $61 and $56 before.

Helped by stronger prices, we have also upgraded our oil production forecasts for Kuwait. According to OPEC figures, Kuwait's crude output rose from 2.71 million b/d in June to 2.79 million b/d in July, and as one of the few OPEC countries with any meaningful spare capacity, could increase further in coming months to help the group meet its aggregate policy goal of lifting output by up to 1 million b/d from pre-summer levels. We expect Kuwait's production to reach 2.85 million b/d by end-year and remain there through 2019. This translates into an increase in oil sector GDP of around 2.5 percent this year and 3.0 percent next.

Real estate sales

Real estate sales in July were the highest in 4 years, at nearly KD 500 million, over double the value from the previous month and triple the value from 1 year ago. The record sales were driven by a rise in activity in all three real estate sectors combined, but most notably the investment sector, which saw a sharp rise in building sales and transactions during the period, followed by the residential sector which also posted strong gains with more than double the sales of June. Prices on the other hand continued on a negative trend, easing further in July, with the exception of the apartment sector index, which has risen moderately (3.8 percent m/m), a sign of improvement in a sector which has been burdened by oversupply and softer demand over the past 2 years. The July surge in sales and activity was likely helped by lower prices, and a possible correction after 3 consecutive months of declines during Ramadan and the early summer months.

Consumer spending growth

Growth in NBK's consumer spending index slowed to 3.5 percent y/y in August from 6.5 percent in July, affected by travel and holidays. The index dropped 2.5 percent on the month, coinciding with Hajj (Islamic pilgrimage) and a 10-day Eid holiday. According to the Directorate General of Civil Aviation, the number of passengers that traveled during Eid-Al-Adha is expected to have reached 542,000, up 52 percent on the same period last year. Year-to-date, the NBK PCE index is down 3.5 percent, though is expected to pick-up upon the end of the summer season and the start of the academic year.

NBK consumer spending index

Consumer spending is projected to continue growing through 2018, albeit at a softer pace than originally expected. A steady expansion in both Kuwaiti and expat employment (better than earlier expectations) should support the spending climate, with further help from low inflation and higher public spending.

Inflation rises

Headline inflation rose to 0.8 percent in July from 0.5 percent in June on the back of higher food prices. Food prices rose 0.8 percent m/m in July and to 1.2 percent y/y from 0.1 percent y/y in June. With food accounting for 17 percent of the CPI basket, July's price rise contributed more than two-thirds of the increase in inflation overall. The pickup in food inflation appears to be stemming from fish and seafood prices, which rose 5.5 percent m/m and 7.8 percent y/y. Meanwhile, deflation in housing services (mostly rents) - which has been the main factor behind low inflation in 2018 - was steady in July at -0.9 percent y/y.

Excluding food and housing, inflation rose to 1.9 percent from 1.7 percent in June. We expect inflation to trend flat-to-higher for the remainder of the year as the pace of decline in rents eases in tandem with some recent improvement in the investment real estate market. Food prices are also showing a modest uptrend. Our forecast is now for inflation to average 0.8 percent in 2018 overall, rising to 2 percent next year.

Credit growth picks

Although still running at modest levels, credit growth increased for a second consecutive month in July, increasing by 2.5 percent y/y (1.7 percent in June). The improvement was due to solid borrowing by both businesses and households, with the former supported by a recent pick-up in project financing. Household borrowing, however, was unusually supported by borrowing through credit cards, which offset a decline - the first since 2012 - in installment loans, which are used for home financing and typically the main driver of household debt. The overall pick-up in credit growth should accelerate towards the end of the year as some large one-off corporate repayments that reduced credit levels in 4Q17 fall out of the annual comparison.

Deposit growth meanwhile eased to 3.9 percent y/y from 4.6 percent in June due to drawdowns in both private and government deposits. Despite rising oil prices, growth in government deposits, saw its seventh consecutive monthly decline, now at -5.0 percent y/y. Government deposits account for 15.7 percent of all deposits from over 17 percent a year ago.

Stock market

Kuwait's All-Share equity index fell 0.6 percent in August, but this was better than the 2.2 percent decline in the MSCI GCC index. Regional stocks in August were affected by both a global sell-off and trade war concerns, which more than offset the positive impact of rising oil prices. Year-to-date (end of August), the Kuwaiti market was up 6.4 percent.

August's trading volume, at KD20 million, was high relative to early in the year and last year, although down from the KD 27 million recorded in July. Strong activity is on the back of positive expectations related to the imminent inclusion of the first tranche of Kuwaiti stocks in the FTSE Emerging Market index due on September 24. The market did suffer its first net outflow of foreign institutional investment this year, likely related to the global sell-off, but net foreign purchases so far this year remain high at above KD100 million. Market capitalization stood at close to KD 29 billion.

NBK ECONOMIC REPORT