SAN JOSE: Nvidia chief Jensen Huang on Tuesday showcased cutting-edge chips for artificial intelligence and new applications for the technology, shrugging off talk of China’s DeepSeek disrupting the market and dangers from US President Donald Trump’s trade wars.

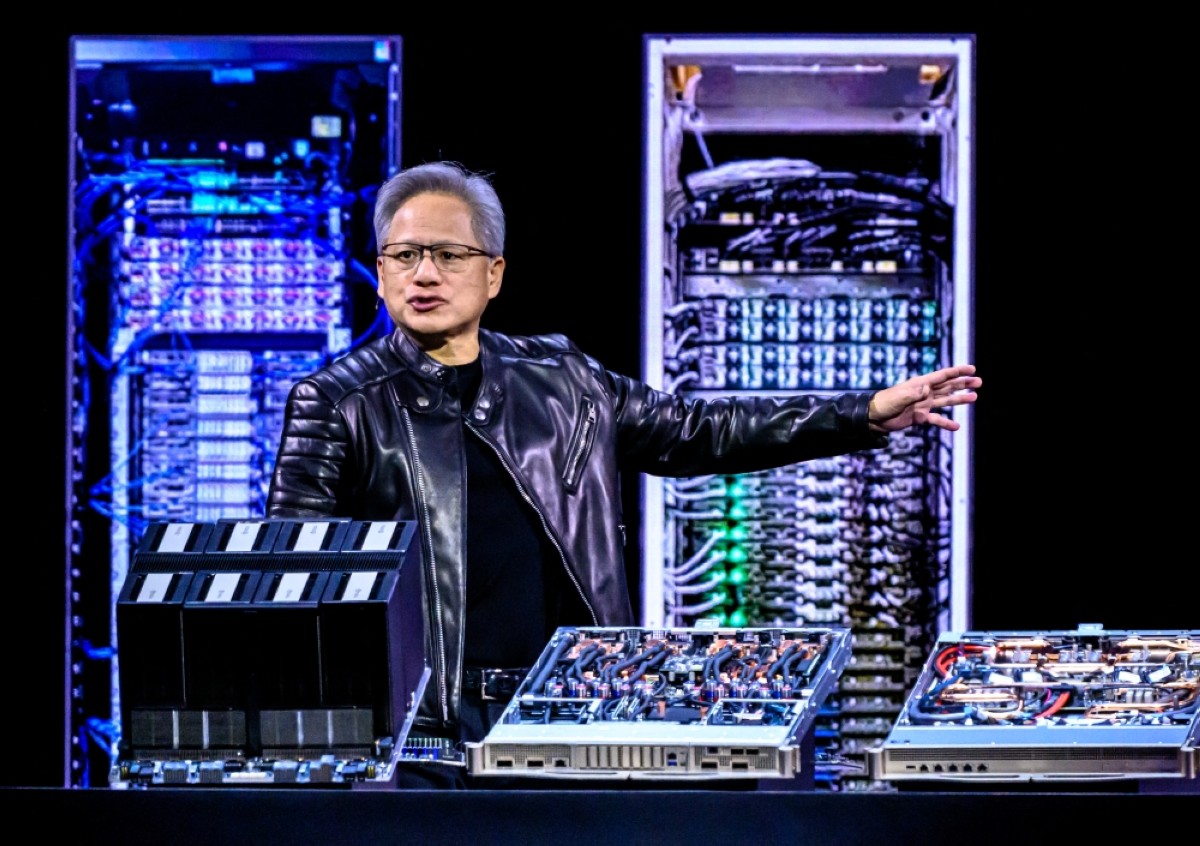

Huang gave a hotly anticipated keynote presentation at Nvidia’s annual developers conference that packed the SAP Center in the Silicon Valley city of San Jose, home of the Sharks NHL hockey team.

Billing the event as an AI "Super Bowl,” the Taiwan-born tech titan was greeted by an audience of more than 20,000 who sat through his two-hour-plus address announcing the company’s latest updates. "The difference is that everyone is a winner at this Super Bowl,” he said, promoting the universal benefits of AI technology.

Huang used the annual speech to unveil developments and tie-ups at the company he co-founded more than three decades ago. Nvidia has seen stratospheric growth, with the AI frenzy stemming largely from the company’s core product: graphics processing units (GPUs). Huang spotlighted the updates to Nvidia’s latest Blackwell line of GPUs, as well as new hardware and software for robotics and telecommunications.

The announcements included a partnership with General Motors focused on developing driverless vehicles that would feature an Nvidia-made, in-vehicle computing system that can deliver up to 1,000 trillion operations per second. He also unveiled a telecoms project, involving T-Mobile and Cisco Systems, where Nvidia will help create AI-ready hardware for wireless 6G networks, the successor to today’s 5G.

The AI boom has propelled Nvidia stock prices to historic levels, though it saw a steep sell-off earlier this year triggered by the sudden success of DeepSeek and the instability of Trump’s tariff battles with key trading partners. Trump has threatened to slap extra tariffs on imports of computer chips to the United States, which will heap pressure on Nvidia’s business, which depends on imported components mainly from Taiwan. High-end versions of Nvidia’s chips face US export restrictions to the major market of China, part of Washington’s efforts to slow its Asian adversary’s advancement in the strategic technology. Against those headwinds, Nvidia stock, one of the most traded on Wall Street, is down more than 17 percent since Trump took office and the release of DeepSeek, an AI model, in January.

China-based DeepSeek shook up the world of generative artificial intelligence with the debut of a low-cost, high-performance model that challenges the hegemony of OpenAI and other big-spending behemoths. Several countries have questioned DeepSeek’s handling of data and believe that the secretive company may be subject to the control of the Chinese government.

Nvidia high-end GPUs are in hot demand by tech giants building data centers to power artificial intelligence, and some say a low-cost option could weaken the Silicon Valley chip star’s business.

But Nvidia and others argue that cheaper AI models will spur their wider expansion, increasing the needs for computing and Nvidia’s technology. "In essence, Nvidia’s chips remain the new oil or gold in this world for the tech ecosystem as there is only one chip in the world fueling this AI foundation... and it’s Nvidia,” said Dan Ives of Wedbush Securities.

Riding the AI wave, Nvidia has ramped up production of its top-of-the-line Blackwell processors for powering AI, logging billions in sales in just months. Huang on Tuesday presented the Blackwell Ultra, an upgraded version, which will be supplanted by yet another line in 2026, the Vera Rubin, a new GPU named after the US astronomer who discovered dark matter.

Nvidia reported it finished last year with record high revenue of $130.5 billion, driven by demand from cloud computing giants including AWS and Microsoft. — AFP