Small cap stocks witness random purchasing

{kind=link}

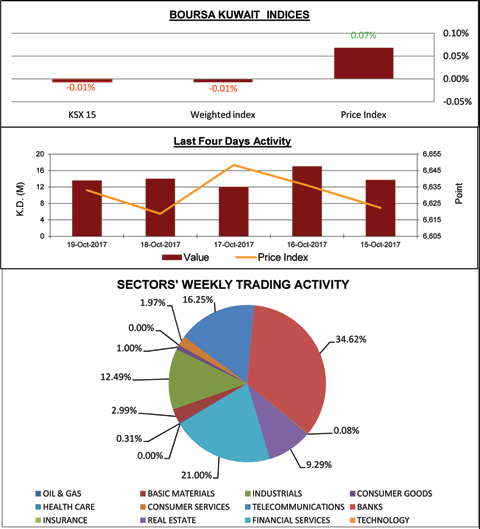

KUWAIT: Boursa Kuwait ended last week with mixed performance. The Price Index closed at 6,633.07 points, up by 0.07 percent from the week before closing, the Weighted Index decreased by 0.01 percent after closing at 431.52 points, whereas the KSX-15 Index closed at 1,004.88 points down by 0.01 percent. Furthermore, last week's average daily turnover decreased by 45.54 percent, compared to the preceding week, reaching KD 14.07 million, whereas trading volume average was 78.87 million shares, recording a decrease of 39.86 percent.

The fluctuation witnessed by the Boursa indices by the end of the week came as a result to the differences in the traders' preferences, as some small-cap listed stocks witnessed random purchasing operations at one end and quick speculative operations at the other end, which positively reflected on the Price Index that was able to end the week with limited gains, while some leading stocks were subject to profit collection operations, which pushed the Weighted and KSX-15 indices to end the week in the red zone.

Boursa Kuwait lost during the last week around KD 65 million of its market capitalization, which reached by the end of the week to KD 28.82 million, down by 0.22 percent of its level at a week earlier, where it reached KD 28.89 billion, to contract by this the market cap gains of the market since the beginning of the year to 13.45 percent compared to its value at end of 2016, where it reached then KD 25.41 billion. (Note: The market cap for the listed companies in the official market is calculated based on the average number of outstanding shares as per the latest available official financial data. Also, the amount of KD 77.28 million was deducted from the total market cap during the last week, which is the market cap of the company that was delisted from the market on Thursday).

The market is witnessing this period a general state of watch for the listed companies results for the nine months of the current year, amid a refrain of some traders from trading, waiting for the listed companies disclosures of its fiscal financial results, which is expected to be declared in the coming days.

As per the daily trading activity, the market declined during the first session of the week as a result to the control of the selling pressures over the trading activity, which was accompanied by the drop in the cash liquidity level to reach its minimum levels during the current month, as it reached KD 13.7 million; and the Price Index closed the session down by 0.09 percent, while the Weighted Index decreased by 0.25 percent, also the KSX-15 Index recorded a daily loss of 0.24 percent. The market was able on Monday's session to realize good gains for its three indices to compensate its previous session's losses, which came as a support from the return of the purchasing activity once again amid concentration on the leading stocks, especially the Banks stock after the disclosure of some banks of good financial results for the nine months of the current year. The Price Index ended the session with a growth of 0.21 percent, while the Weighted and KSX-15 indices recorded gains of 0.35 percent and 0.46 percent respectively.

On the mid-week session, the market continued recording gains for the second consecutive session, however relatively limited, supported by the random purchasing operations executed on some stocks of different weights, amid a larger concentration on the small-cap stocks being traded at low values, which was reflected on the cash liquidity that dropped by the end of the session by around 30 percent, as the Price Index closed by the end of the session up by 0.19 percent, while the Weighted Index increased by 0.06, and the KSX-15 Index's gains reached 0.13 percent.

On Wednesday's session, the market returned to the red zone once again, as all its indices ended the session with some losses, amid a noticeable activity of selling pressures and profit collection operations that concentrated on small-cap stocks, which was negatively affected on the Price Index in particular, to end the session with losses reached 0.45 percent, while the Weighted Index losses reached 0.20 percent , and the KSX-15 Index recorded a very limited loss of 0.004 percent. On the end of week session, the market ended its session with mixed closings for the three indices, whereas the Price and Weighted Index were able to realize limited increase by the end of the session reached 0.22 percent and 0.03 percent respectively, while the KSX-15 Index went against the current and recorded by the end of the session a drop of 0.35 percent.

For the annual performance, the Price Index ended last week recording 15.40 percent annual gain compared to its closing in 2016, while the Weighted Index increased by 13.53 percent, and the KSX-15 recorded 13.54 percent growth.

Sectors' Indices

Seven of Boursa Kuwait's sectors ended last week in the red zone, four recorded increases, whereas the Health Care sector's index closed with no change from the previous week. The Basic Materials sector headed the losers list as its index declined by 0.87 percent to end the week's activity at 1,287.64 points. The Telecommunications sector was second on the losers' list, which index declined by 0.59 percent, closing at 596.09 points, followed by the Insurance sector, as its index closed at 1,103.29 points at a loss of 0.45 percent. The Banks sector was the least declining as its index closed at 961.88 points with a 0.08 percent decrease.

On the other hand, the highest gainer was the Oil & Gas sector, achieving 2.12 percent growth rate as its index closed at 1,034.77 points. Whereas, in the second place, the Real Estate sector's index closed at 955.03 points recording 0.75 percent increase. The Consumer Services sector came in third as its index achieved 0.57 percent growth, ending the week at 923.83 points. The Consumer Goods sector was the least growing as its index closed at 1,016.84 points with a 0.08 percent increase.

Sectors' Activity

The Financial Services sector dominated a total trade volume of around 160.43 million shares changing hands during last week, representing 40.68 percent of the total market trading volume. The Real Estate sector was second in terms of trading volume as the sector's traded shares were 25.51 percent of last week's total trading volume, with a total of around 100.60 million shares.

On the other hand, the Banks sector's stocks were the highest traded in terms of value; with a turnover of around K.D 24.35 million or 34.62 percent of last week's total market trading value. The Financial Services sector took the second place as the sector's last week turnover was approx. KD 14.77 million representing 21 percent of the total market trading value. -- Prepared by: Studies & Research Department - Bayan Investment Co.